Overview of Deeming

So, as mentioned, it is a way to determine the income of your financial assets, but why only for financial assets?

Well, contrary to other income sources, such as rent from an investment property, which is stable and consistent, the income from your financial assets varies according to its performance on the markets.

If the economy is performing well, the market goes up and, therefore, you receive a substantial return on your assets. On the other hand, if the markets go down, your asset’s performance goes down with it, and you may even have a loss.

Deeming is a way of calculating a set rate of income independent of what they actually earn, which eventually results in a stable age pension rate, as this deemed income is used in the income test.

This is the primary reason why deeming is used. We’ll discuss the other benefits of deeming later on in this post, but first, we’ll look at some examples of what is considered a financial asset.

The main types of financial assets

- Saving accounts and term deposits

- Managed investments, loans and debentures

- Listed shares and securities

- Some income streams (for example, your super)

- Some gifts you make

How Deeming Works

First, you need to determine the total value of your financial assets, and then apply the rules depending on your living status (as shown below).

| Deeming rate | ||

| Single | 1.75% on the first $51,800 | 3,25% on the rest |

| Couples (at least one gets pension) | 1.75% on the first $86,200 (combined assets) | 3.25% on the rest |

| Couple (no one gets pension) | 1.75% on the first $43,100 (your own and your share of joint assets) | 3.25% on the rest |

Once you have calculated this, you then get the deemed income, which will be considered in your income test.

Okay, let’s pause for a moment before we lose you completely! We’ll take a look at some examples so that you can gain a better understanding of how much this can actually be.

Income Per Fortnight

| Financial Asset Value | Single | Couple (at least one gets pension) |

| $100,000 | $95 | $75 |

| $200,000 | $220 | $200 |

| $500,000 | $595 | $575 |

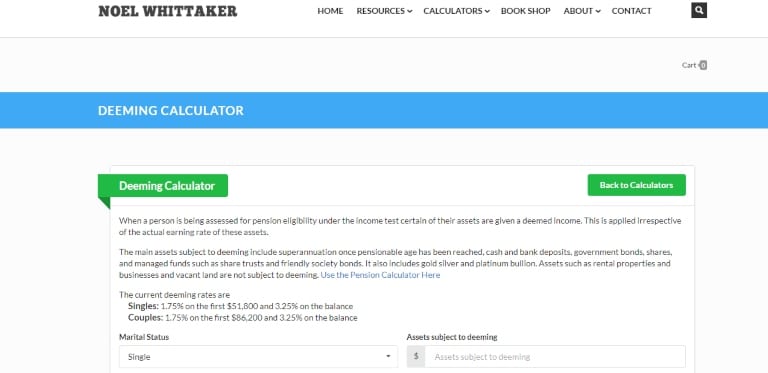

You can take a look at Noel Whittaker’s Deeming Calculator for an easier way of figuring this out.

We have to admit, these numbers are actually smaller than what we initially expected. This also leads us to the discussion about the benefits of deemed income.

Benefits Of Deeming – An Example

One of the significant benefits is that if your financial assets perform successfully, more so than the deeming rate, then this interest will not be considered as income.

Let’s view this example. Here, we are taking the same numbers as in the previous example; however, we only need to look at the couple to make it more transparent.

We took 6% of the return because according to Canstar, the top-performing super funds had a return of 6.42% in the last year. Why super funds?

Well, most Australians have some money in a super fund, and this is a financial asset. Therefore, most Australians are affected by these deeming rules.

| Financial Asset Value | Deemed income for Couple | Really income if 6% return, rounded |

| $100,000 | $75 | $231 |

| $200,000 | $200 | $462 |

| $500,000 | $575 | $1,154 |

As you can see, the actual income would be bigger, and it may have a more significant effect on your age pension rate.

This is because the more income you have, the less age pension you get – well, after a certain limit, of course. So, yes, using the deemed income instead of the real income is a more realistic and mindful approach.

Other Benefits Of Deemed Income

There are several more benefits associated when using the deemed income. As mentioned previously, deeming creates a set rate of income. This essentially means that your income is considered stable, even if the performance of the investments varies.

Furthermore, this means that the more payments you receive, the age pension remains stable, too. This, in our opinion, makes life much easier. It is much easier to do budgeting if your age pension stays stable, wouldn’t you agree?

And the final benefit we wish to mention is that it allows you to choose the best investments conforming to your needs. You don’t need to base your choice of investments on how they may affect your age pension payments!

Cases When Investments Underperform

In this case, you can get an exemption. If you get it, the actual income from the investment will be counted as income in the income test; and yes, this income can be $0.

Usually, you have to apply for your exemption with one exception – in the case of if there is an investment company collapsing, and a lot of investors are affected, there may be a group exemption applied to all investors, and you don’t have to apply for one as an individual.

Some examples of what may be exempt include:

- Failed financial investment

- Some super if it is fully preserved or inaccessible

- An account that only contains money from a National Disability Insurance Scheme Package

Here is what will not be exempt:

- Shares with negative returns

- Companies or funds that are having short term problems

Who decided if you can get an exemption?

The Minister for Families and Social Services, and once it is granted, it will continue until the reason for it no longer exists.

Now you know the important information about deeming, and you should now be able to estimate your deemed income for the income test.

If you would like to know how this may affect your age pension, then we suggest that you watch or read the information we shared about the income test and assets test. You can also check out our simple overview of the Age Pension in Australia!

We hope that we were able to explain this concept of deeming in an uncomplicated manner. Please let us know what your thoughts are in the comments below, and check out our Free Learning or YouTube Channel for more retirement-related content.